Many companies believe that once their Income Tax Return (ITR) has been successfully filed, their compliance responsibilities are complete.

However, if an income tax scrutiny notice is issued several months later, the typically does not begin by asking about tax planning strategies or computation methods.

Instead, the first requirement is usually documentary evidence supporting the figures reported in the return.

With the increasing use of technology in tax administration, the Income Tax Department now relies extensively on data analytics and cross-verification of information from multiple sources.

These sources may include:

- Financial statements

- GST records and returns

- TDS and TCS returns

- Annual Information Statement (AIS)

- Statement of Financial Transactions (SFT)

- Other third-party information available with the tax authorities

As a result, businesses that maintain complete, accurate, and well-organized documentation are generally in a stronger position to respond effectively to scrutiny notices and departmental queries.

This guide explains the key documentation practices businesses can implement in advance to strengthen their compliance framework and remain prepared before any income tax scrutiny notice is received.

Income Tax Scrutiny Doesn’t Start with Taxes—It Starts with Documents

An income tax scrutiny is primarily a process of verifying evidence rather than recalculating taxes.

While the figures reported in the Income Tax Return (ITR) are important, the Income Tax Department generally expects businesses to support those figures with proper documentary evidence.

During scrutiny proceedings, businesses may be asked to explain or substantiate:

- Income reported in the Income Tax Return

- Business expenditure claimed

- Tax deductions and exemptions

- Loans, borrowings, and investments

- Bank transactions

- Related-party transactions

- Purchase of fixed assets

- Statutory compliance records

- Books of accounts and supporting records

Businesses that maintain complete documentation throughout the year are generally able to respond to scrutiny more efficiently than those that begin searching for invoices, agreements, reconciliations, and supporting records only after receiving a notice.

Preparing documentation after scrutiny begins is often time-consuming and increases the risk of inconsistencies or missing evidence.

Filing the Income Tax Return is only one aspect of tax compliance.

Equally important is maintaining organized records that enable every figure reported in the return to be supported whenever required during scrutiny, assessment, or verification by the Income Tax Department.

Why Businesses Are Selected for Income Tax Scrutiny

Selection for income tax scrutiny does not necessarily indicate tax evasion, fraud, or incorrect reporting by a business.

The Income Tax Department follows a risk-based assessment system and uses technology-driven data analytics to identify cases that may require further verification.

Information reported by taxpayers is compared with data received from various government departments, financial institutions, and other reporting entities.

A business may be selected for scrutiny for reasons such as:

- Mismatch of information across different tax forms and statements

- High-value financial transactions

- Unusual deductions, exemptions, or loss claims

- Significant fluctuations in reported income compared to previous years

- Information received from other government departments or reporting agencies

- Risk parameters prescribed by the Central Board of Direct Taxes (CBDT)

- Cases arising from surveys, searches, reassessments, or investigations

- Consequential action based on findings from earlier assessments

In many cases, scrutiny is initiated simply because certain transactions or reporting patterns require additional verification.

Businesses that maintain complete documentation and accurate supporting records are generally better equipped to respond to such enquiries and demonstrate the correctness of the information reported in their Income Tax Returns.

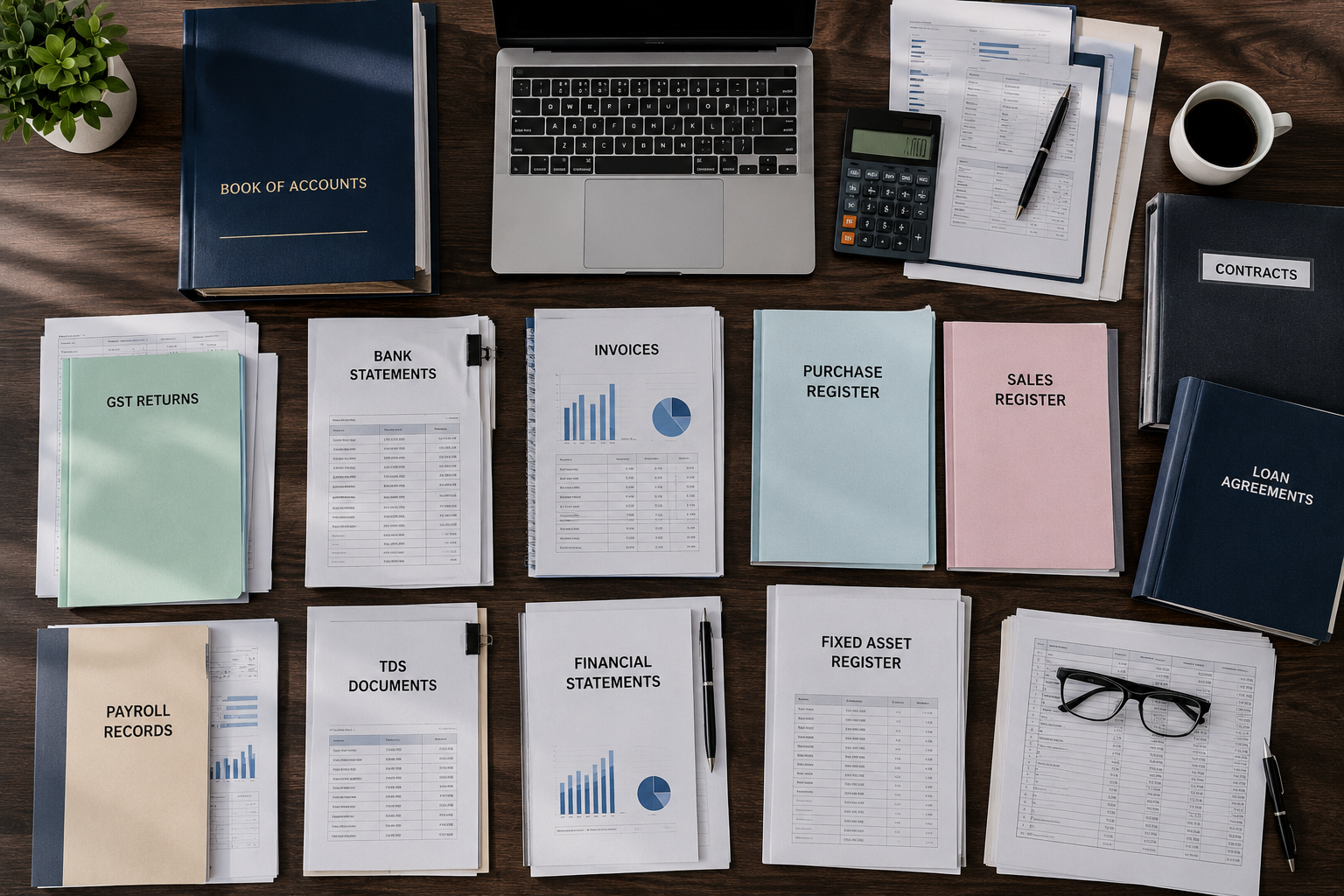

Documents Commonly Requested During Income Tax Scrutiny

During an income tax scrutiny, the Income Tax Department may request various financial and supporting documents to verify the information reported in the Income Tax Return.

Keeping these records organized and readily accessible can significantly reduce the time required to respond to departmental queries and support the figures reported in the return.

| Document | Reason for Relevance During Scrutiny |

|---|---|

| Books of Accounts | Primary accounting records supporting the financial statements and tax return. |

| Sales Register | Verification of turnover reported in the books and Income Tax Return. |

| Purchase Register | Support for purchases and business expenditure claimed. |

| Bank Statements | Verification of receipts, payments, and financial transactions. |

| GST Returns | Reconciliation of turnover, purchases, and tax-related information. |

| Financial Statements | Verification of reported profits, assets, liabilities, and financial position. |

| Tax Computation | Explanation of taxable income calculations and adjustments. |

| Business Invoices | Supporting evidence for sales and expenditure reported. |

| Supporting Documents for Expenses | Verification that business expenses are genuine and incurred for business purposes. |

| TDS Records | Verification of tax deducted at source and related claims. |

| Payroll Registers | Support for salary and employee-related expenditure. |

| Fixed Asset Register | Verification of fixed assets and depreciation claims. |

| Loan Agreements | Explanation of borrowings and interest expenditure claimed. |

| Customer and Vendor Contracts | Evidence supporting commercial transactions and contractual arrangements. |

| Investment Records | Verification of investments and related income. |

| Tax Audit Report (where applicable) | Support for tax disclosures, reconciliations, and statutory reporting. |

Preparing these documents well before any scrutiny notice is received allows businesses to respond more efficiently, minimize delays, and demonstrate that the figures reported in their Income Tax Return are supported by complete and reliable documentation.

Why Books of Accounts Alone Are Not Enough

Many businesses assume that maintaining accounting software and properly recorded books of accounts is sufficient for income tax compliance.

In reality, the books of accounts represent only one part of the documentary evidence required during an income tax scrutiny.

Tax authorities generally expect businesses to support accounting entries with underlying documents that establish the nature, purpose, and authenticity of each transaction.

For example, where a business claims expenditure on professional consultancy services, the Income Tax Department may request:

- Letter of engagement or consultancy agreement

- Invoice issued by the consultant

- Proof of payment

- TDS deduction and payment details, where applicable

- Bank statement evidencing the payment

- Correspondence or records demonstrating that the consultancy services were actually provided

Similarly, where marketing or advertising expenses are claimed, supporting records may include:

- Agreement with the advertising or marketing agency

- Campaign invoices

- Payment proofs

- Work completion reports or deliverables

- Campaign reports, screenshots, or other evidence in the case of digital marketing activities

During scrutiny, the objective is not merely to verify that an expense has been recorded in the books.

The Income Tax Department may also seek evidence that the expenditure was actually incurred, relates to the business, and is supported by adequate documentation.

For this reason, businesses should maintain supporting documents alongside their accounting records so that every significant transaction reported in the books can be substantiated whenever required.

Business Expenses That Require Strong Supporting Documentation

During an income tax scrutiny, business expenses are generally expected to be supported by adequate documentary evidence.

Maintaining complete records helps demonstrate that an expense was genuinely incurred for business purposes and supports its allowability under the Income-tax Act.

| Expense Type | Supporting Documentation |

|---|---|

| Travel Expenses | Air or train tickets, hotel invoices, travel approvals, boarding passes (where applicable), and proof of payment. |

| Professional Fees | Engagement agreement, consultant invoices, TDS records, and payment proofs. |

| Marketing & Advertising | Agency agreement, campaign invoices, campaign reports, work deliverables, and payment records. |

| Office Rent | Rent agreement, rent receipts, and bank payment evidence. |

| Salary Expenses | Employment contracts, payroll registers, salary sheets, and bank transfer records. |

| Consultancy Charges | Letter of engagement, consultancy agreement, invoices, correspondence, and payment proofs. |

| Maintenance & Repairs | Invoices, bills, service reports, and work completion records. |

| Interest Expense | Loan documents, bank certificates, interest statements, and repayment schedules. |

| Capital Investments | Purchase invoices, installation reports, asset register entries, and payment records. |

Proper documentation strengthens the credibility of business expenditure by demonstrating that the expense was genuine, properly recorded, and incurred wholly for business purposes.

Maintaining these records throughout the year enables businesses to respond more effectively during income tax scrutiny, audits, and departmental verification while reducing the time required to gather supporting evidence.

When Do GST Records Become Relevant During Income Tax Scrutiny?

Although the Income-tax Act and the GST law operate independently, the financial information reported under both statutes is closely connected.

During an income tax scrutiny or assessment, tax authorities may compare GST records with accounting and financial records to verify the accuracy and consistency of the information reported.

Common areas of comparison include:

- Turnover reported in GST returns with revenue disclosed in the financial statements

- Purchase records under GST with business expenses recorded in the books of accounts

- Tax invoices with accounting entries

- GST reconciliation statements with the books of accounts

Significant differences between GST records and income tax records may result in additional questions during assessment and require further explanations or supporting documentation.

Maintaining consistency between GST returns, financial statements, and accounting records helps businesses demonstrate the reliability of their reported figures and reduces the likelihood of avoidable discrepancies.

Regular reconciliation of GST data with books of accounts throughout the financial year can simplify the assessment process and minimize the need for extensive clarifications during income tax scrutiny.

Documentation Checklist Every Business Should Review Before an Income Tax Inquiry

Businesses should not wait until they receive an income tax scrutiny notice to organize their records.

Maintaining a structured documentation system throughout the year enables faster responses during assessments, e-Proceedings, and departmental verification while reducing the risk of missing supporting evidence.

Financial Documentation

- General Ledger

- Trial Balance

- Profit and Loss Statement

- Balance Sheet

- Cash Book

- Journal Entries

- Fixed Asset Register

Banking Documentation

- Bank Statements

- Loan Ledgers

- Interest Certificates

- Payment Acknowledgements

Taxation Documentation

- Income Tax Returns

- Tax Computation Statements

- Tax Audit Report (where applicable)

- TDS Statements

- Tax Challans

- GST Returns and Related Records

Vendor Documentation

- Purchase Orders

- Vendor Agreements

- Purchase Invoices

- Payment Confirmations

Employee Documentation

- Payroll Registers

- Salary Slips

- Employment Agreements

- PF and ESI Records (where applicable)

Agreements & Contracts

- Customer Agreements

- Vendor Contracts

- Service Agreements

- Lease Agreements

- Consultancy Contracts

Compliance Documentation

- Board Approvals (where applicable)

- Statutory Registration Certificates

- Reconciliation Statements

- Internal Compliance Review Records

Organizing and digitally indexing these documents makes it easier for businesses to retrieve records quickly during income tax assessments and e-Proceedings.

A well-maintained documentation system not only improves response time but also strengthens the business’s ability to substantiate transactions, explain financial information, and demonstrate overall tax compliance.

Example: A Business That Faced Difficulties Due to Inadequate Documentation

Consider a technology services company that correctly prepared and filed its Income Tax Return, including consultancy fees paid to several external professionals.

During the scrutiny process, the accounting entries and invoices were available.

However, the company was unable to produce some consultancy agreements and supporting correspondence relating to the services received.

Although the consultancy expenses had genuinely been incurred, the absence of complete supporting documentation resulted in additional queries from the Income Tax Department, delays in the assessment process, and increased compliance efforts.

If the company had maintained properly organized consultancy agreements, invoices, payment proofs, and related correspondence throughout the year, verifying the expenditure would have been considerably more straightforward.

Common Documentation Issues Faced by Businesses During Income Tax Scrutiny

| Documentation Issue | Potential Consequence |

|---|---|

| Missing invoices | Difficulty substantiating business expenditure. |

| Unsigned or incomplete agreements | Questions regarding the authenticity of transactions. |

| Poor record management | Delays in responding to scrutiny notices. |

| Incomplete reconciliations | Additional queries and verification by the department. |

| Unsupported deductions | Requirement for further explanations and documentary evidence. |

| Missing payment records | Difficulty establishing that business transactions actually took place. |

| Inconsistencies between GST records and books of accounts | Extended discussions and additional reconciliation during scrutiny. |

In many scrutiny proceedings, challenges arise not because the tax computation is incorrect, but because businesses are unable to produce sufficient documentary evidence to support the figures reported in their Income Tax Return.

Maintaining organized records throughout the year helps businesses respond more efficiently to departmental enquiries and reduces the likelihood of unnecessary delays during assessment.

Documentation Practices for Effective Income Tax Scrutiny Preparation

Businesses should establish documentation procedures throughout the financial year instead of waiting until an income tax scrutiny notice is received.

A structured documentation process helps ensure that financial records remain accurate, supporting documents are readily available, and responses to departmental queries can be prepared efficiently.

| Frequency | Documentation Activities |

|---|---|

| Monthly |

|

| Quarterly |

|

| Year-End |

|

Following a structured documentation schedule throughout the year enables businesses to identify gaps early, maintain complete supporting records, and significantly simplify the process of responding to income tax scrutiny.

Well-organized documentation not only strengthens tax compliance but also reduces the time, effort, and uncertainty involved when responding to departmental notices, assessments, and e-Proceedings.

How Professional Documentation Reviews Help Businesses Prepare for Income Tax Scrutiny

Many businesses conduct periodic documentation reviews with the assistance of professional advisers, such as JackRabbit Consultants, well before any income tax scrutiny or assessment begins.

The objective of these reviews is to identify documentation gaps early and strengthen the company’s overall compliance framework before receiving a notice from the Income Tax Department.

A professional documentation review typically focuses on:

- Validation of supporting documentation

- Verification of consistency between financial records and supporting documents

- Assessment of overall tax compliance documentation

- Review of agreements, invoices, reconciliations, and statutory records

- Preparation for income tax scrutiny and departmental assessments

- Identification of documentation deficiencies before the verification process begins

JackRabbit Consultants assists businesses in evaluating whether their financial records, supporting documents, reconciliations, and compliance files are sufficiently organized to support the information reported in their Income Tax Returns during scrutiny.

The objective is not simply to ensure that returns have been filed correctly, but also to verify that every significant transaction can be supported with appropriate documentary evidence whenever required by the tax authorities.

Conducting periodic documentation reviews helps businesses strengthen their compliance processes, reduce the risk of documentation-related queries, and improve preparedness well before any scrutiny notice is issued.

Before the Income Tax Department Requests Your Documents…

Preparing for an income tax scrutiny involves much more than filing an Income Tax Return on time.

Every figure reported in the return should be supported by complete and well-organized documentary evidence, including books of accounts, reconciliation statements, invoices, agreements, payment records, and other relevant business documents.

An Income Tax Return explains what has been reported. Proper documentation explains why those figures are correct and provides the evidence required during scrutiny.

Businesses that maintain a structured documentation system throughout the year are generally better equipped to respond to scrutiny notices, departmental enquiries, and e-Proceedings without unnecessary delays.

Well-maintained records not only simplify the verification process but also reduce the time and effort involved in gathering supporting documents after a notice has been received.

Many businesses choose to periodically review their documentation and compliance processes with the assistance of professional advisers such as JackRabbit Consultants to strengthen their preparedness before any scrutiny or assessment takes place.

Ultimately, the strongest defence during an income tax scrutiny is not created after receiving a notice—it is built through consistent documentation, timely reconciliations, disciplined record management, and robust compliance practices maintained throughout the financial year.