Many board members believe DIR-3 KYC filing is an annual requirement—but this misunderstanding can lead to serious consequences in 2026, where non-compliance may result in DIN deactivation.

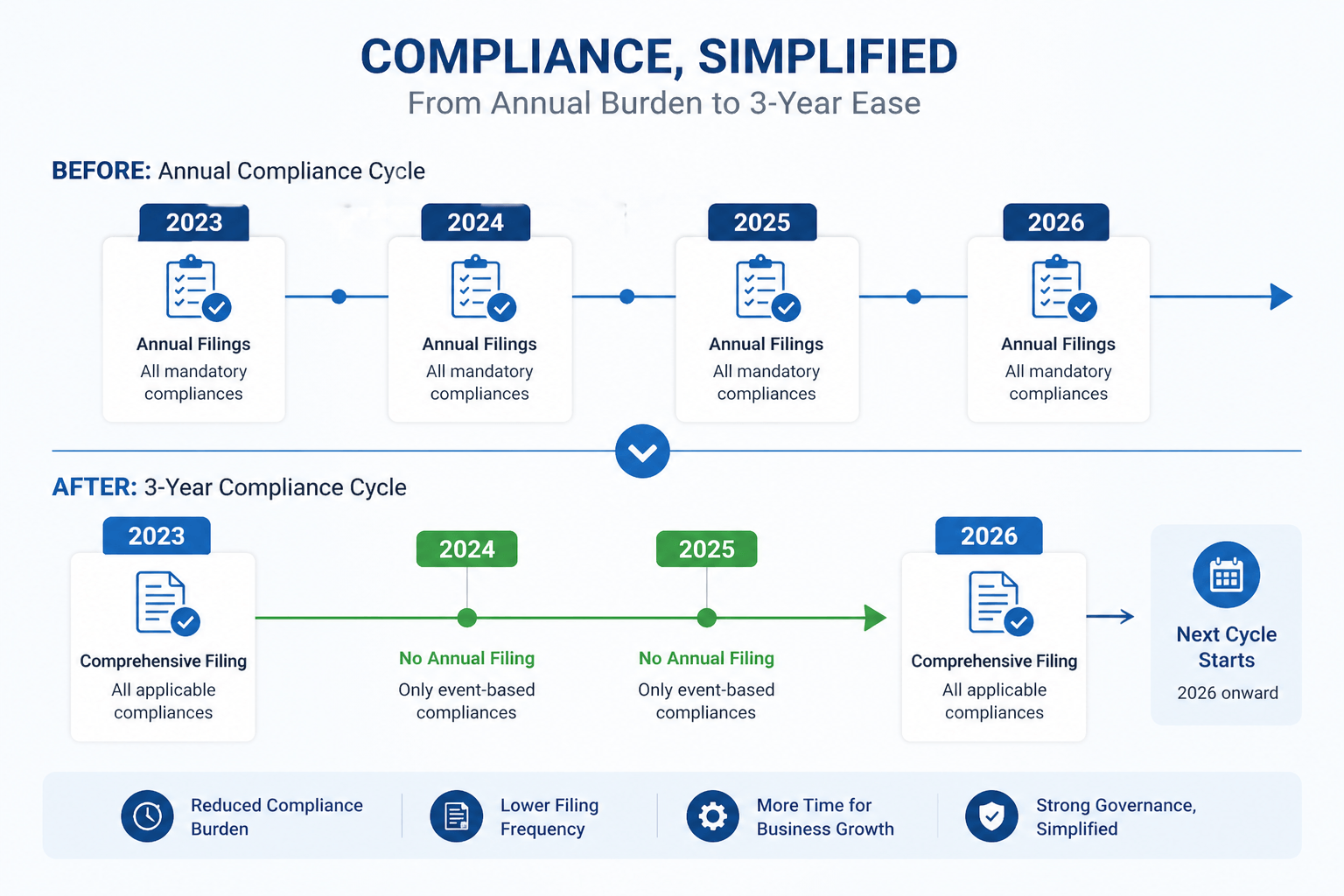

The MCA has significantly revised the filing procedure. With the transition from annual filing to a three-year compliance cycle, confusion has arisen regarding whether filing is required in the current year and what happens in case of non-compliance.

This issue is not about complex procedures—it is about misinterpreting applicability under the updated 2026 rules.

How DIR-3 KYC Laws Have Been Amended in 2026

The Ministry of Corporate Affairs (MCA) has updated the Companies (Appointment and Qualification of Directors) Rules, 2014 through the Amendment Rules, 2025, effective from 31 March 2026.

Structural Change

- Old Rule → Annual filing (every year)

- New Rule → Once every 3 financial years

Compliance Mechanism

A director holding a valid DIN must file DIR-3 KYC:

- Once every 3 consecutive financial years

- Before 30 June of the applicable cycle year

In simple terms: Annual filing is no longer applicable. DIR-3 KYC now follows a structured 3-year compliance cycle.

Who Needs to File DIR-3 KYC in 2026?

This is the most critical compliance confusion point. Your requirement depends on your last filed KYC year.

| Scenario | Filing Required in 2026? | Reason |

|---|---|---|

| Director filed KYC in FY 2022–23 | ✅ Yes | 3-year cycle ends in 2026 |

| Director filed KYC in FY 2023–24 | ❌ No | Cycle not completed |

| Director filed KYC in FY 2024–25 | ❌ No | Still within cycle window |

| New director added in 2025–26 | ✅ Yes | First compliance filing required |

| DIN inactive but not surrendered | ✅ Yes | Reactivation required via KYC |

Key Takeaway: Not all directors are required to file in 2026. Filing depends entirely on the completion of the 3-year cycle.

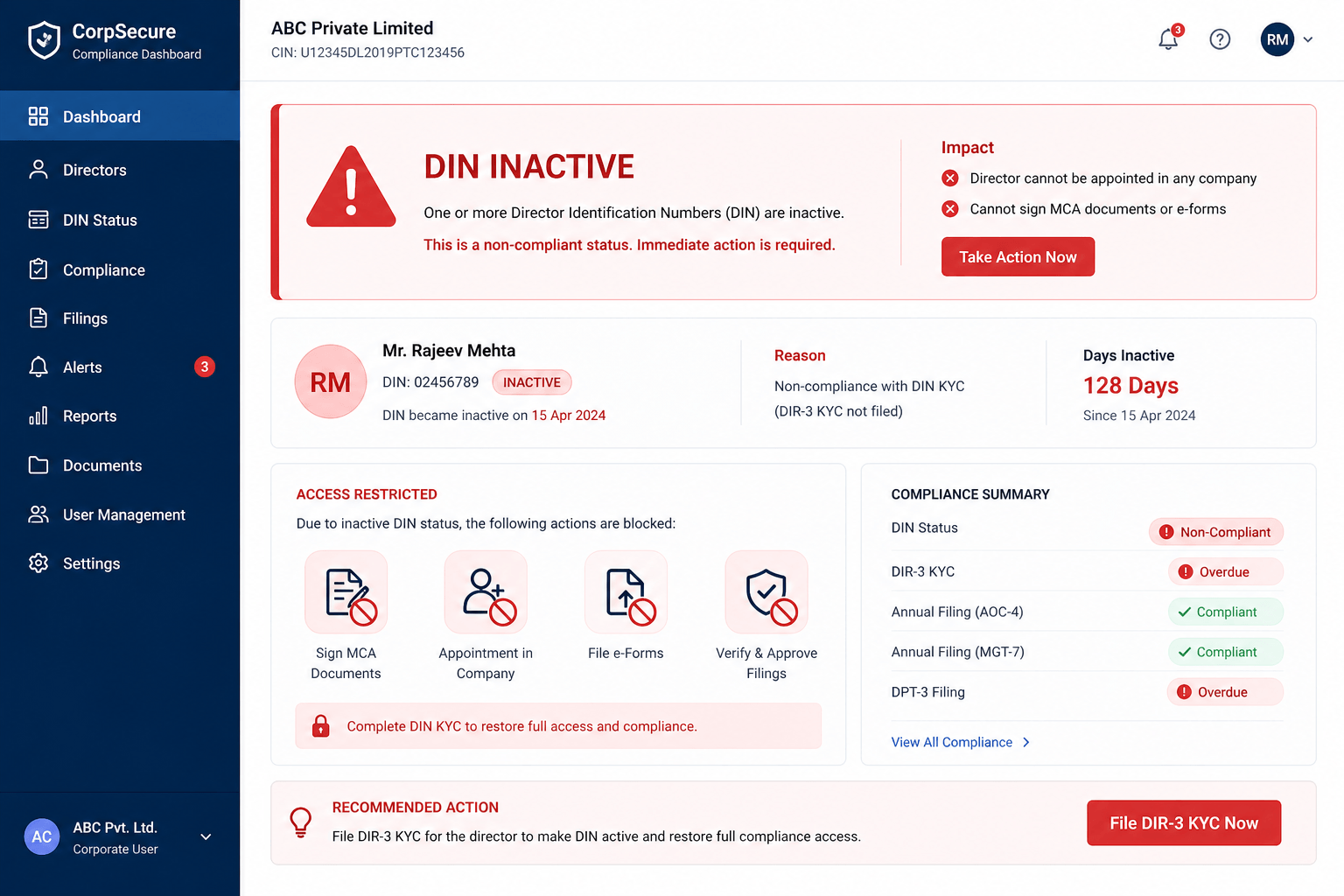

What Happens If DIR-3 KYC Is Missed?

Missing DIR-3 KYC is not just a procedural lapse—it triggers system-level restrictions on your DIN.

A. DIN Deactivation (Immediate Impact)

- DIN status changes to Inactive

- Director cannot sign MCA filings

- Cannot approve statutory documents

This effectively blocks the director from performing legal company functions.

B. Compliance Breakdown at Company Level

- Annual return filings get stuck

- ROC submissions get rejected

- Board approvals become invalid

In practice, the company’s compliance workflow comes to a halt.

C. Financial Penalty Impact

- ₹5,000 fixed late fee per DIN

- Additional ROC adjudication penalties in serious cases

In enforcement scenarios, penalties may increase depending on the duration of delay and compliance history.

Practical Example: How Directors Become Complacent About Filing Their Documents

A common pattern seen among directors in 2026:

Director believes:

“I filed last year, so there’s no need for another filing.”

However, under the revised system:

- Last filing does not necessarily update the compliance cycle correctly

- MCA system tracks status as of 31 March

- Directors may suddenly become liable to file

Consequences

- DIN becomes inactive

- Delay in company ROC filings

- Emergency filing required with ₹5,000 penalty

This may appear uncommon, but it is one of the most frequent compliance failures in the current system.

Why Most Directors Fail in DIR-3 KYC Compliance

Despite being a mandatory requirement, failures usually occur due to identifiable reasons:

-

Ignorance about the new 3-year system

- Many directors still follow the outdated annual filing approach

-

Lack of compliance management system

- Small and mid-sized firms lack proper DIN tracking mechanisms

-

Over-reliance on consultants

- Assuming consultants will handle all compliance obligations

-

Outdated contact information

- OTP failures due to inactive email or mobile numbers

DIR-3 KYC vs DIR-3 KYC-Web (Key Difference)

| Type | Use |

|---|---|

| DIR-3 KYC (old e-form) | Previous system (not used for routine filing now) |

| DIR-3 KYC-Web | Current MCA V3 portal filing system |

Major Change in 2026

- Full online submission platform

- OTP-based verification for login

- DIN and DSC not required for routine filings

This simplifies the filing process. However, dependency on accurate contact information has increased significantly.

Common DIR-3 Compliance Issues Committed by Company Directors

Most compliance failures arise due to avoidable mistakes:

- Assuming KYC needs to be done annually

- Lack of awareness about MCA notifications

- Not updating mobile numbers or email IDs before filing

- Uncertainty about the exact filing timeline

- Assuming DINs are always active

These errors directly increase the risk of DIN becoming inactive.

How Should Directors Comply With DIR-3 KYC Requirements in 2026?

A structured compliance system is essential.

Compliance Framework for Directors

- Maintain a DIN cycle tracking system

- Track the last filing year for each DIN

- Set internal alerts for the June deadline

- Update contact details immediately after any change

- Regularly verify DIN status on the MCA portal

Basic Requirement: If you cannot quickly answer — “What was the year of my last DIR-3 KYC?” — your compliance tracking system is insufficient.

Insider Insights: The Real Reasons for Compliance Failure

In reality, most DIR-3 KYC default cases do not arise due to technological issues.

Instead, they occur due to:

- Inability of directors to monitor compliance cycles

- Lack of awareness regarding rule changes

- Assumption that compliance will be managed automatically

The shift from a “yearly compliance practice” to a “compliance cycle system” is the key transformation in 2026 compliance understanding.

Structured advisory firms such as JackRabbit Consultants often implement internal DIN monitoring dashboards to eliminate such gaps before they result in penalties.

Conclusion

DIR-3 KYC compliance in 2026 has evolved from a procedural formality into a cycle-based eligibility control mechanism for directors.

The shift from annual filing to a three-year compliance cycle has changed the core issue from “filing delay” to “cycle awareness failure.”

Structured directors experience no disruption, while those relying on memory or outdated assumptions risk DIN deactivation and penalties.

The compliance requirement itself is simple—but failure to manage it correctly leads to significant regulatory consequences.